Why Emerging Managers matter: Access Capital Partners’ conviction built over three decades in European small cap buy-outs

04-06-2026 Small cap buy-outs

Introduction

Emerging managers are one of the most compelling ways to access the small cap buy-out segment where pricing discipline, alignment of interest and operational value creation matter greatly to produce outperformance.

In that context, emerging managers are often the part of the market where incentives are strongest and execution is sharpest.

A practical definition of emerging managers

The term emerging manager is sometimes used too broadly, often reaching out as far as third generation funds.

The market is both deep and highly dynamic, with more than 60 new teams emerging each year, a trend that continues to gain momentum in an environment where operational value creation and disciplined underwriting are increasingly critical to generating strong returns. Within that universe, three broad profiles tend to stand out.

The first is the below-the-radar manager, often operating through deal-by-deal structures, and now transitioning to a more institutional format. The second is the spin-off, where experienced professionals leave an established platform or financial institution to build an independent franchise. The third is the newly formed team, where seasoned investors and often entrepreneurs come together around a clear sector angle, sourcing advantage or investment discipline.

Emerging managers at the core of small cap buy-outs

The small cap buy-out market remains the most attractive and resilient segment of private equity, underpinned by strong structural advantages. Its appeal is further enhanced by the outperformance potential of first-time funds, providing another compelling layer of opportunity.

This small cap environment also lends itself naturally to buy and build strategies, driving rapid and meaningful value creation.

“For us, emerging managers are not a style shift from mainstream small cap buyouts, they are often where the small cap market is most entrepreneurial, most aligned and most capable of generating differentiated returns.”

Agnès Nahum & Philippe Poggioli, Managing Partners at Access Capital Partners

The performance case: why emerging managers can outperform

The case for emerging managers is sometimes framed as an argument about outperforming established firms. We believe the most compelling perspective is structural. Emerging managers are attractive because the conditions around their early stage often produce better alignment of interest and the highest degree of motivation.

Not all emerging managers succeed in raising a debut fund. In fact, the majority fails to do so. Those who do succeed are usually battle hardened by tough fundraising and have made short term sacrifices to maximize long term gains. Access Capital Partners itself will only invest in a small proportion of its emerging manager deal flow, making each individual fund commitment a high conviction / rigorous due diligence exercise.

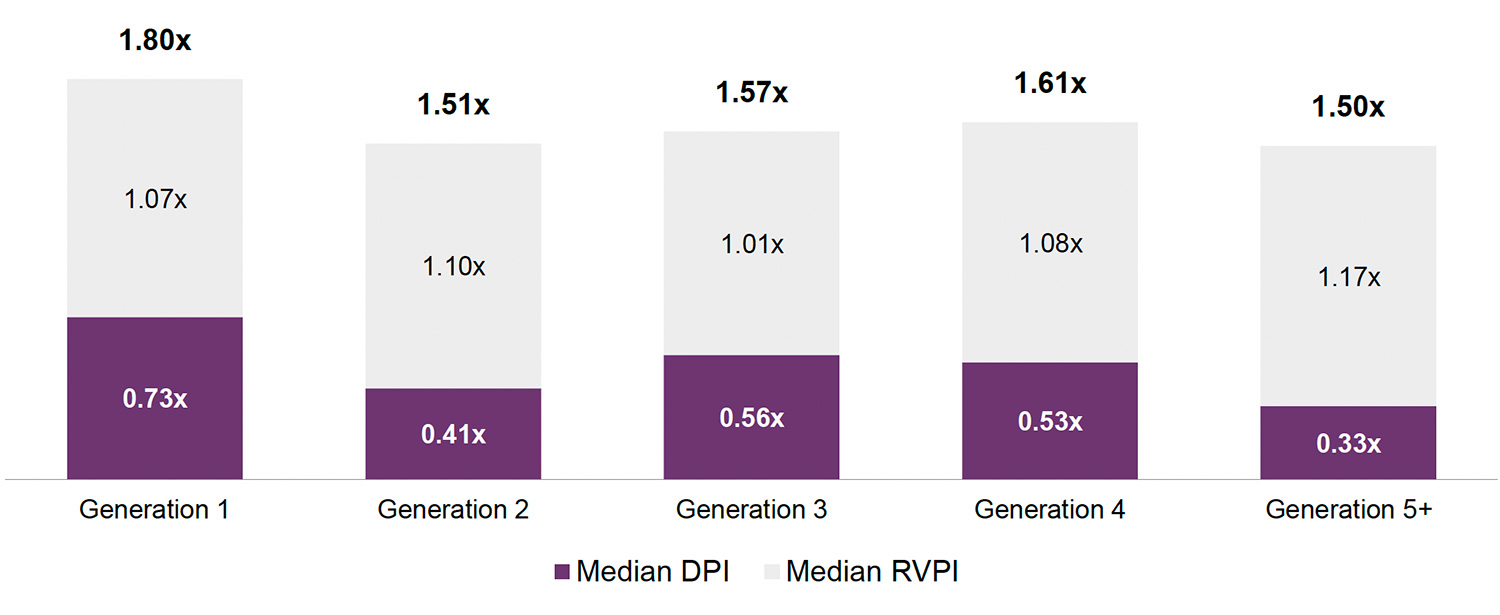

First generation funds outperforming later generations

Median TVPI by fund generation

Source: Preqin, vintages 2015-2022, sample of 308 funds

In our experience, four drivers are particularly important.

1. A fully dedicated team

Emerging managers are typically focused on a single strategy and a smaller number of investments. It means senior professionals are not diluted across multiple products, legacy portfolios or internal committees with competing priorities. Time is spent on sourcing, underwriting, portfolio monitoring and value creation, not on managing organisational complexity.

2. Stronger alignment through meaningful GP commitment

Alignment is not a slogan in first-time or early-generation funds, it is part of the economic reality. These teams are building reputation, track record and future fundraising capability. GP commitment is often meaningful in relative terms, and the reputational stakes are high. That can translate into disciplined investment selection and a higher degree of hands-on management than may established GPs.

3. Differentiated sourcing and sector depth

The best emerging managers are rarely generalists by default. Many originate from a sector, operating network or sourcing niche where they can access proprietary or lightly intermediated opportunities.

In the small cap segment, that differentiation is critical. Competitive tension can be lower, but only for managers who genuinely know where to look.

4. Concentrated portfolios with higher conviction

Portfolio concentration increases responsibility, but it also sharpens selectivity. That concentration can accelerate capital deployment and bring forward value crystallisation.

In emerging managers portfolios, the first exit alone can materially underpin the economics of the fund within two to three years.

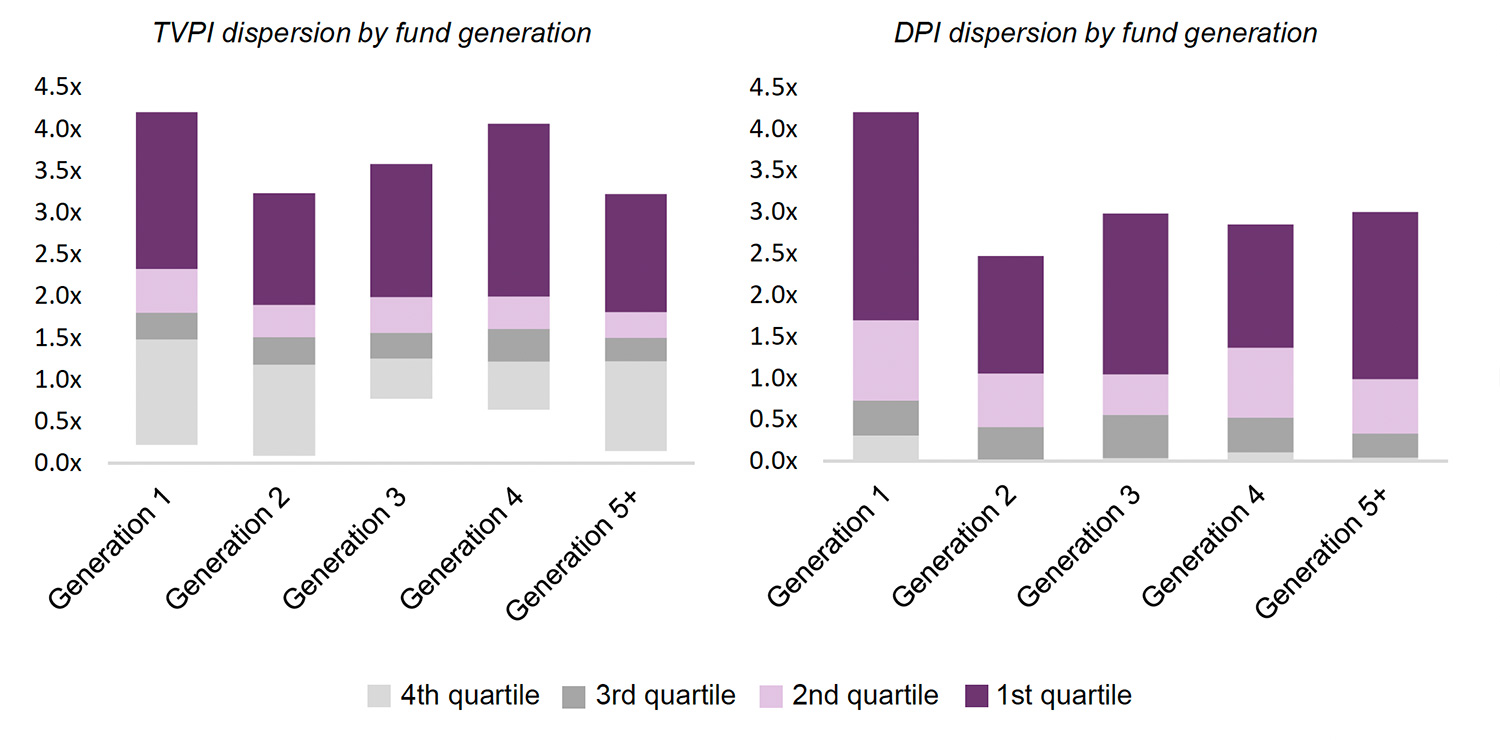

Why emerging managers are particularly well suited to a fund of funds model

A fund of funds approach is particularly relevant in emerging managers because the opportunity set is broad, but dispersion can be high.

Increased dispersion of first-time funds compared to older generations

Source: Preqin, vintages 2015-2022, sample of 308 funds

Finding the next stars requires structured selectivity

Successful emerging manager selection is a repeatable discipline.

Emerging managers are therefore not only an access opportunity, they are a selection challenge. The value lies in recognising quality before it becomes consensus.

Cornerstone LPs can improve institutional readiness

This significant investor position can support fund structuring, governance, reporting and operational readiness from the outset.

For early-generation teams, institutionalisation is part of the investment case, not an administrative afterthought.

Diversification is a structural advantage

A fund of funds approach mitigates individual manager dispersion.

This is particularly valuable in concentrated underlying funds, where manager quality is high, but outcomes can be more dispersed.

ESG can be a structural advantage when embedded early

Institutional investors increasingly expect ESG to be built in from the onset. For earlygeneration managers, this creates both a challenge and an opportunity. The challenge is obvious: teams are small, resources are finite and reporting requirements are rising. The opportunity is equally clear: with no legacy infrastructure to unwind, managers can build a framework that is proportionate, decision-useful and linked to value creation.

This is particularly important in small cap buy-outs, where governance, human capital, supply-chain resilience, energy efficiency and compliance processes often have direct operational impact. The best emerging managers embed ESG into diligence, ownership planning and board-level follow-up.

Conclusion

Emerging managers represent a compelling opportunity because they are often closer to the fundamental drivers of superior performance: alignment, focus, sourcing, pricing discipline and active ownership.

In European small cap buy-outs, those qualities are especially relevant. This is a segment where differentiated sourcing matters, where portfolio concentration can be an advantage and where institutional quality can be fostered by a strong cornerstone LP.

In that sense, emerging managers are a lens through which to identify where entrepreneurial energy and investor alignment are most powerfully combined.